In my last article on April 4, I introduced a framework for understanding the market (ambiguity vs. uncertainty) as well as a few of the debt market measures that, should they normalize, signal a re-opening of the commercial real estate debt and equity markets. Since then, the Federal Reserve released new term sheets for its various lending facilities. Three things to note under these new terms:

- The Fed’s term asset lending facility will accept legacy AAA-rated private-label CMBS

- Its corporate bond credit programs will purchase the debt of companies that are later downgraded to below investment grade status.

- One of the facilities will be able to purchase high yield bond ETF shares

Following these announcements, credit market conditions have improved in these targeted areas and to a lesser extent in related credit markets. It is important to remember that all pricing across financial markets are interrelated by risk arbitrage relationships. That is, if two different securities have the same risk exposures, then they should be priced the same way. Any time these relationships are violated, there is a potential investment opportunity.

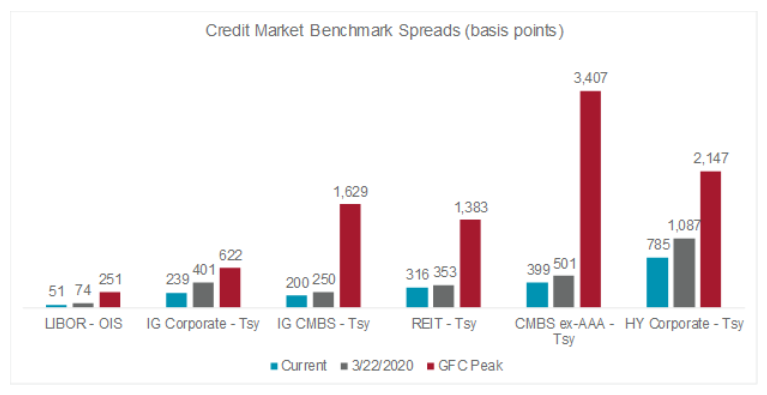

Before we look in detail at the more recent movement in credit benchmarks, it’s important to note that while we are faced with enormous economic challenges that in some ways already exceed those posed by the Great Recession, so far this is not a financial crisis. The figure below compares a range of real estate debt market benchmark spreads at different times. At no time, in the last several months have levels of distress even remotely approached those observed during the Great Financial Crisis (GFC) nor will they.

This does not mean we haven’t experienced problems or won’t continue to experience them. Liquidity and issuance deteriorated (or even ground to halt) in commercial paper, corporate bond and commercial real estate debt markets. In the last several weeks, liquidity and issuance have recovered in each of these sectors, particularly investment grade corporate bonds. Improvement in the commercial paper markets has reduced some of the impetus for corporations to draw down their revolvers and consequently revolver balances have stabilized in the last weeks. This in turn has helped improve liquidity conditions in the interbank market with the spread between LIBOR and the federal funds rate narrowing modestly.

Despite these improvements, however, spreads remain significantly wide compared to levels observed in 2019. The LIBOR spread at 51 basis points (bps) is still significantly higher than the 2019 average of 9bps. Investment grade corporate bond spreads have declined significantly from their March peak, but they are still 115bps wide of pre-crisis numbers. The same is true – indeed more true – for investment grade CMBS (122bps wider vs 2019), REIT debt (195bps), non-AAA CMBS (233bps) and most of all high yield corporate bonds (377bps). It is difficult to disagree with debt investors who are demanding larger risk premia in a significantly higher risk environment.

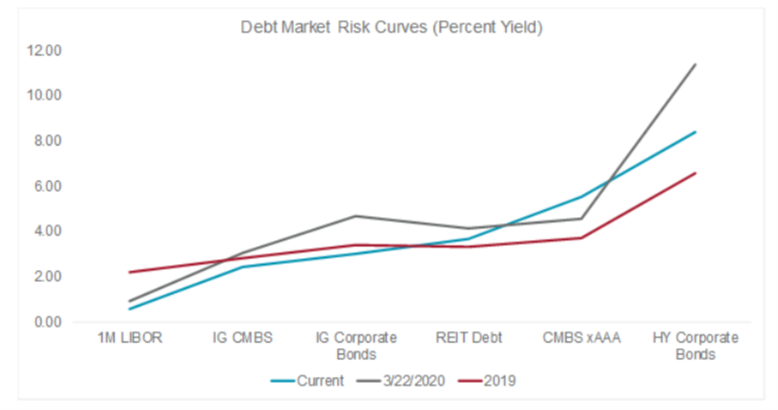

Fortunately for borrowers, all-in borrowing costs typically matter much more than the spreads, and for the most part, borrowing costs are now at, near or, below pre-crisis levels.

One-month LIBOR averaged 2.23% in 2019, but now stands at just 57bps and will likely decline further. For LIBOR-based borrowers, this translates to lower all-in financing costs to the extent they are not subject to LIBOR floors. Investment grade CMBS corporate bonds are both now trading inside 2019 levels. REIT debt, however, is still trading slightly outside of 2019 levels and historically wide of corporate bonds. Given the overlapping risk exposure between the issuers of investment grade corporate bonds and the tenants in REIT-owned properties, yields on these securities tend to trade in lockstep. In fact, given that rent payments are higher in the capital stack than unsecured bond payments, REIT debt typically trades inside of corporate bonds. For these reasons, it seems likely that the historical relationship will reassert itself with REIT debt yields compressing. This has positive implications for CRE debt market broadly.

Yields remain significantly higher in the lower rated CMBS markets and for high yield corporate debt. Indeed, the CMBS xAAA index somewhat understates the continued distress in lower tranches: secondary market conduit spreads for below investment grade tranches continue to trade at spreads just below 1,500bps compared to ~800bps in February. These yields reflect continued illiquidity, and particularly in the CMBS market, mean that even if there are now buyers for the AAA pieces, securitization cannot move forward lest the financial intermediary be left holding the junk paper. But the dynamic won’t last—it is only a matter of time until investors who reason that BBB- rated paper is desirable at yields north of 10% emerge.

In the near-term, however, we should look for CRE lending conditions to improve for lower risk deal profiles, while originations for higher risk hotel, retail and transitional assets will remain strained. Sustained low debt costs will relieve upward pressure on cap rates for core properties, while an overall improvement in debt market liquidity will ultimately translate to equity investors returning to the market. In the case of both the equity and debt markets, activity will continue to be restrained by elevated uncertainty. The success of European nations and select U.S. states as they look to reduce COVID-19 restrictions will be critical in dictating the outlook. And positive developments will point towards a quicker return of activity and thus price discovery.